The time has come for the container-shipping industry to join the digital revolution. Digital opens the door for carriers to strengthen their direct relationships with end customers, further reduce their costs (including for fuel, vessel operation, and customer service), and pursue new revenue streams beyond traditional shipping services.

Only a few leading carriers have applied digital technologies toward enhancing their commercial and operational activities. Box tracking, empty-container repositioning, document management, network design, and pricing are among the activities that these carriers have started to digitalize.

Although the rewards of a digital transformation can be significant, so are the challenges to making it happen. To succeed, carriers must adopt a structured approach to defining a digital vision and integrating new technologies, capabilities, and mindsets into their traditional way of working. It is not too late to get started. The industry is still in the early stages of digitalization, and most carriers have yet to achieve significant progress. Carriers that approach a digital transformation with the right ambition, resources, and scale can leap to the forefront of adoption. Within 18 months, they can achieve a step change in their digital capabilities that strengthens their competitive advantage. Quick wins are achievable within 12 months.

Rough Seas Demand Digital Adoption

In BCG’s November 2016 report Sailing in Strong Winds: The New Normal in Global Trade and Container Shipping, we discussed the industry’s then-current challenge: slow growth in global demand coupled with a persistent oversupply of vessel capacity. Although global container demand did improve in 2017, moderate long-term growth projections combined with a new round of vessel purchases indicate that overcapacity will remain in the range of 6% to 9% in 2020.

Even as the economic challenges of the new normal persist, carriers face an increasing threat from digital attackers. A variety of players—including both traditional logistics players and new entrants—are adopting digital technology to provide seamless, end-to-end services. If these companies’ business models succeed, carriers run the risk of losing direct contact with some of their most profitable customers—primarily small and midsize freight forwarders and beneficial cargo owners (known as BCOs). In this scenario, the carrier’s role could be reduced to providing commoditized ocean freight services.

One of the strongest threats is from players that are adopting digital technology as the basis for an assetless business model that lets them compete with a much lower cost base. Recognizing the opportunity, e-commerce giant Amazon has obtained a license to operate as an assetless cargo forwarder between China and the US. Startups are also gaining traction. For example, Flexport is a technology-based freight forwarder that, as of October 2017, had attracted more than $200 million in venture capital investment. Flexport is not alone in attracting venture capital. In the past six years, more than $3.3 billion has been invested in digital startups in the shipping and logistics sector.

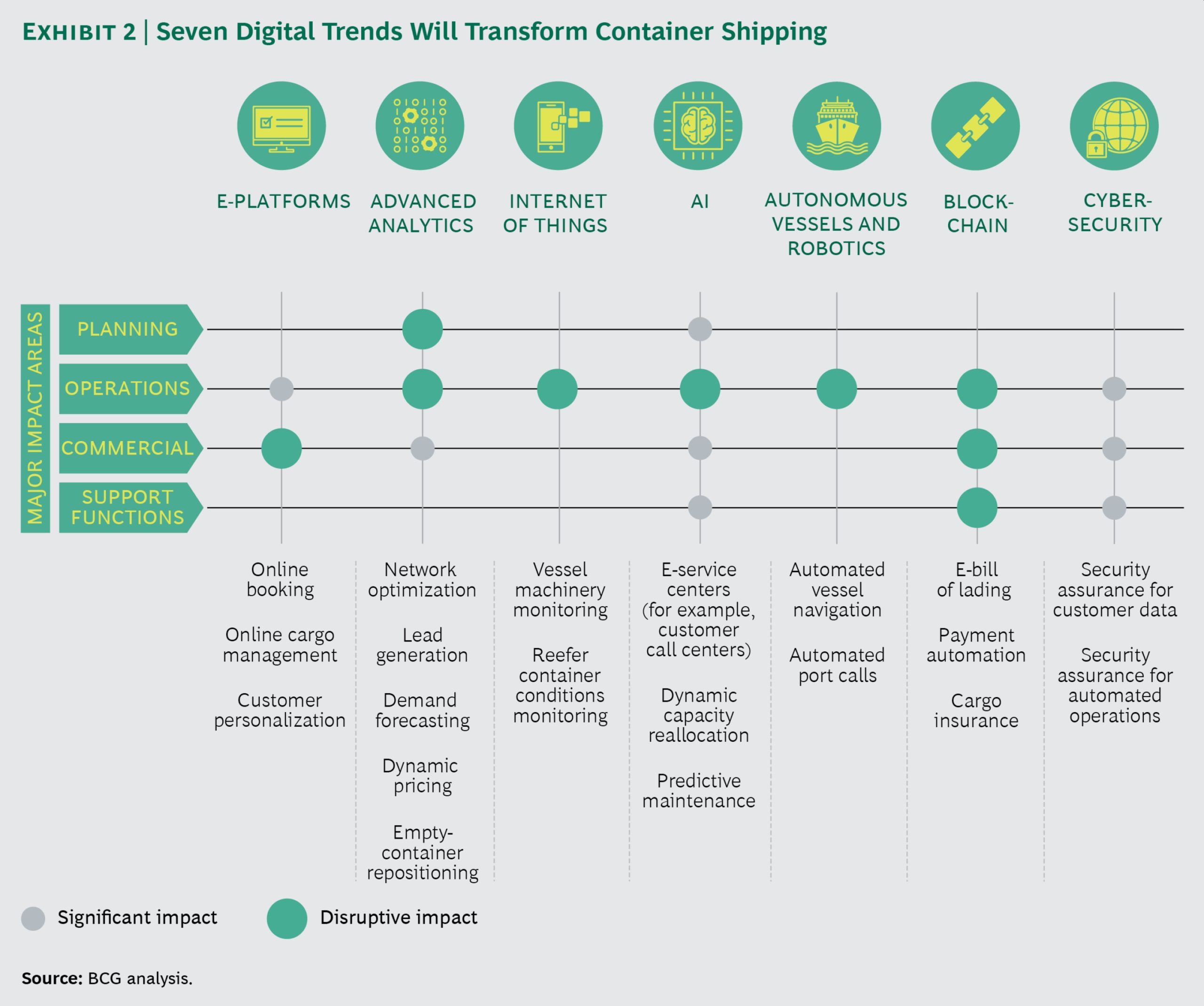

Fortunately, carriers have many opportunities to apply digital technology—not only to maintain their direct customer relationships with acceptable costs but also to improve their operations and grow their businesses. Seven digital trends have emerged as especially valuable in the shipping industry. (See Exhibit 2.) These trends are contributing to performance improvements across the full scope of carriers’ operations.

More: BCG.COM