CE Banking Outlook presents key challenges and individual factors impacting the banking industry in Central Europe. It covers banking sectors in 8 CE countries: Bulgaria, the Czech Republic, Croatia, Hungary, Poland, Romania, Slovakia and Slovenia.

Although the performance of the banking sector in Central Europe (CE) is shifting up a gear as lending growth accelerates and asset quality improves, profitability is still well below pre-crisis levels. With low interest rates driving margin compression and a rising regulatory burden, banks need to improve operating efficiency.

The digital maturity of banks in CE countries varies greatly but digitalization is a strategic priority for all. It can not only provide a key avenue for banks to reduce their cost to serve, it is also an imperative that enables them to keep pace with the expectations of customers who are increasingly online and mobile. M&A activity has picked up visibly in CE in recent years, with growing activity in Southern markets (Hungary, Slovenia and Romania), supported by stabilizing asset quality and often involving non-bank buyers (such as private equity funds and insurers). Uneven profit distribution in the banking sector and the advantages of scale will drive further consolidation.

While Europe’s economic recovery is expected to slow in 2016 and 2017, and the UK’s Brexit vote has increased uncertainty, conditions are expected to remain relatively favourable for CE banks. The Economist Intelligence Unit (EIU) is forecasting GDP growth for the CE region to be 2.8% for the whole of 2016, and 2.7-3.0% in 2017-18 (1.3-1.5 percentage points above the eurozone). This relatively healthy economy has led a faster recovery of loan growth in CE to 3.4% y/y in 2015 (3 p.p. above Euro area) and should allow a further pick up to 5.0% y/y in 2018.

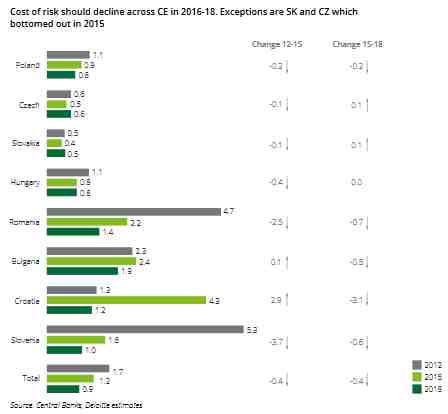

Asset quality has also been improving, with the non-performing loan (NPL) ratio in CE down from a peak of 11.0% in 2013 to 8.8% in 2015 and is expected to fall to a level of 7.0% in 2018. As the region’s recovery progresses, the disparities between the leading countries in the north (Poland, the Czech Republic and Slovakia) and those in the south (Hungary, Romania, Bulgaria, Croatia and Slovenia) are expected narrow.

…

Dr Grzegorz Cimochowski, Lead Partner in Strategy Consulting in Central Europe, Deloitte, Vincent Bastid, CEO,

More in: Deloitte CE Banking Outlook 2016